|

Realizing that everyone is in a different place financially, I offer ideas for every situation. Whether you need to get going or are thinking about how you'll finish, this is a fun message that offers direction and confidence. This "masterclass" was delivered in front of a few hundred Vector Marketing Managers. They created a word cloud to express how they felt at the end of my talk. I hope it creates the same feelings for you. Disclaimer: I'm just a dude that really digs talking about money. Please seek the advice of a licensed fiduciary (which I also talk about in the video). Enjoy!  Check out Deciding to Thrive chapters 8 and 9 for my financial road map. 100% of profits/proceeds/every penny from both books go to help children with dyslexia learn to read. Let's leave the world better than we found it. #leaveitbetter Author John WassermanDad | husband | speaker | entrepreneur | children's dyslexia center board member | top sales trainer |

10 Comments

Advice on how to build your resume while in school. Also, creating a vision and a lifestyle to position yourself to land that all important first "real job" out of college.

In this episode of the Changing Lives podcast, host Dan Casetta and guest John Wasserman discuss numerous important concepts for success in business and life, including:

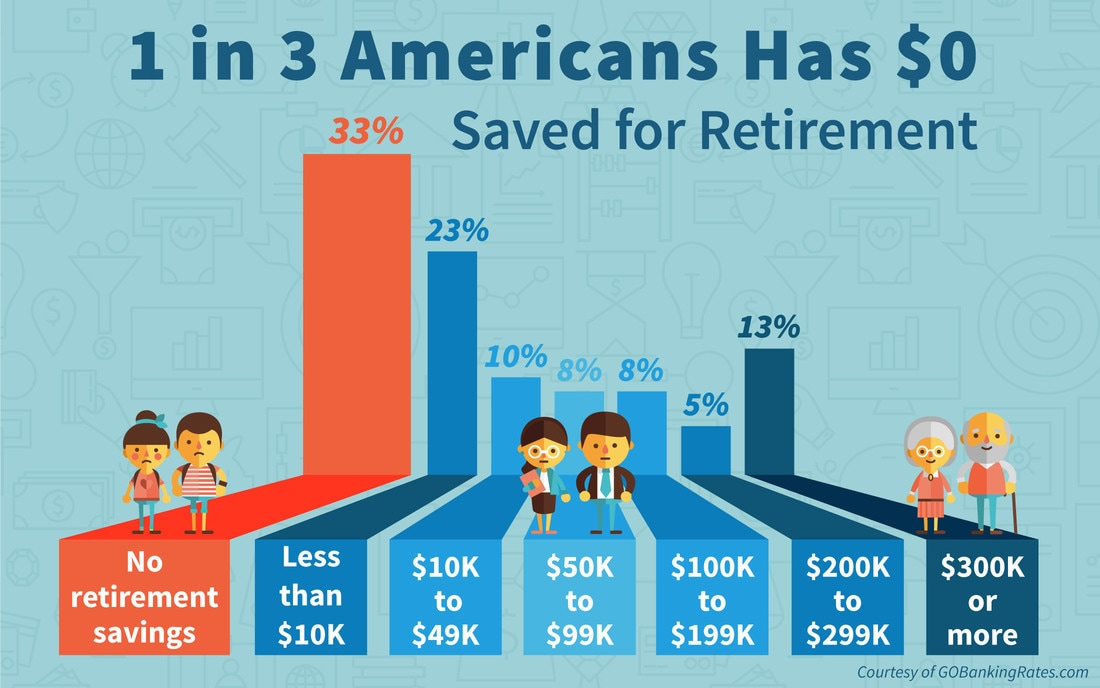

• The importance of reaching out for guidance and support • The pivotal nature of business analysis to move any organization along a trajectory towards success • John’s acronym APE: Analyze, Plan, Execute • Taking control of your personal growth, and the effect on your life • Getting past the feeling of being “burnt out” • And a whole lot more! "You’ll see exactly why and how John Wasserman strives to leave everyone he meets and everyplace he ventures a little better because of his presence and influence. Please enjoy getting to know my long-time colleague, competitor, and friend, John Wasserman." - Dan Casetta  It's a new year and time for a renewed commitment to financial fitness. Setting financial goals can be intimidating. I love setting them and I know how important it is, but at times, I find myself asking "How" questions. Like, "Ok, great goal, now how in the world am I going to do this?" However, it's far more powerful and motivating to ask "Why" questions. As in, "Why do I want to do this?" "How" is a question that's bound to bring up negative feelings. Instead of getting you excited, it can leave you deflated. On the other hand, knowing your "Why" is what's going to help you figure out how. Your "Why" will also keep you energized when you encounter setbacks. There's nothing magical about it. It's a matter of perspective. Knowing why you want to do something shifts your perspective from negative to positive. Instead of getting that sinking feeling in your stomach because you're asking, "How am I ever going to be able to do this?" you'll be buoyed up by knowing, "I have to do this because...". And the more compelling the reason, the harder you will fight to acheive your goal. So, as author Simon Sinek put it best, Start With Why. Here are 3 money tips to kickstart your year: 1. Put Your Financial Goals in Writing Once I come up with the amount I want to invest in various accounts (i.e. retirement accounts, annuities, real estate, etc.), one of my favorite things to do is to write my total investment goal for the year on a sticky note and put it on my bathroom mirror. This forces me to stay focused. Each time I move money to an investment, I subtract it from my total goal. I used to do this with sales goals, and I find it works just as well for financial goals. It keeps me motivated to reach certain benchmarks that I mentally set for myself. For example, reaching $X by the end of the month or quarter. You can use this same method for paying off a credit card or building up an emergency fund. 2. Set Up Automatic Investments Just about every bank or financial institution can help you set up an automatic investment account. Simply put, if you want to max out your Roth IRA at $5500 this year (2017), you can set up your account to transfer $458.33 per month (X 12 months = $5500) to your IRA account. For those 50 or older you can max out at $6500 (or $541.67 per month). You can also set a reminder on your phone a couple of days in advance to help you remember when the transfer is about to take place. You don't have to max it out, so if you can only do $100 or $200 per month, do it. Your 70-year-old self will thank you. Another way to set up auto investing is to select a percentage of your pay each week to transfer to a savings account that you plan to use for investments. The wealthiest savers in the world save 40% of their paychecks, however most experts will recommend at least 10-15%. Heck, you could start at 3% for now. Make it your goal to increase that by 1-2% every 4 months until you feel comfortable investing 10% of each paycheck. Or, if you feel more comfortable transferring the money manually, set a reminder on your phone that goes off every Saturday morning with your target % and make the transfer.  3. Find Money to Invest It's safe to say, this is important. Your future, your retirement, and the lifestyle you dream about...it all comes down to your habits now. Whether you are on top of your game or you feel strapped for cash, there are some things you can do to invest more this year. Here are a few suggestions to find money.

Myth #1: To make a great change in your life, you must change who you are. Not so. You must become more completely who you already are." - Rick Smith, The Leap: How 3 Simple Changes Can Propel Your Career from Good to Great Ahh...the first impression...a mere 90 seconds to win them over or, perhaps...it's over. So what do people say to themselves when they meet you? Do they say, there's something about this person that I really like? Whether you are trying to get a great deal on a Martin LX1E acoustic-electric guitar with a solid Sitka spruce top, mahogany high-pressure laminate back and sides, with a warm satin finish or you're in the first of a series of 'dream job' interviews or even asking someone out on a date (perhaps to join you around a glowing fire while you jam on your new guitar in celebration of your latest greatest career move), you need to establish a connection. Research shows that you have about 90 seconds to make a favorable impression. Here are 3 keys to making a positive, truly memorable, connection. 1. The Initial Greeting

2. Rapport

3. Communication that Makes a Difference

Avoid these pitfalls:

One last interesting tip: 'Eye Cues' for detecting lies.

In closing:

Check out John's books The No Shorts Book and Deciding to Thrive.   Starting in my early teens, I mowed lawns, delivered newspapers, and worked in restaurants. When I had money, I quickly found ways to spend it. I was 22 years old when I became a full time entrepreneur. Saving and investing were the furthest things from my mind. For my 23rd birthday, I bought myself a Toyota MR2. A hot little mid-engine two seater with T-tops. My payments were $500 per month. It turned out to be terrible in the snow. So living in the northeast, naturally I "needed" to lease a Nissan Pathfinder SUV with payments of $350 per month. I had two cars and the monthly payments totaled more than my apartment rent. Eventually I got bored with those vehicles, so I bought a $65,000 Hummer H2. I put ½ down and financed the rest. My payments were $1500 per month, but I paid it off in one year. Sounds awesome so far! But…I had little money saved. I wasn’t building wealth at the rate that I could. Most people put off saving and investing, so I felt like I was in good company with my slow start. After a couple of solid sales years, I finally got smart. I started taking money and investing much more seriously. I devoured dozens of books, magazines, and audios on money and wealth building. I started investing $100 at a time, funding IRAs, SEPs. A little here, a little there. It ads up fast. The same thing used to happen to me with spending... a little here, a little there and you’re like…oh my…did I really spend that much? Since those days, I’ve learned that when it comes to your future the car that you drive is not the vehicle that will get you to the finish line. Here's a quick run down of what I've learned from all those books on building wealth as well as my own experiences (mistakes and course corrections). 5 keys to building your financial future: 1) Be an owner. Owning shares of stocks means you are part owner (a share holder) of that company. What about the risk? For millennials, at your age, there is virtually no risk in stocks or mutual funds. If you are older, a fiduciary can help you navigate the stock market based on your risk tolerance. Ask your bank if they have a licensed fiduciary you can talk to. In my book Deciding to Thrive there are two chapters on money and investing to guide you through it all. 2) Pay yourself first. Your future retired self that is. At least 10% of your gross pay each week (15% if you are starting later in life). If you invest it into a tax deferred retirement account like a Traditional IRA you won’t feel the pay cut as much since you will be able to write off the investment (at the time of this writing up to $5500 per year, $6500 per year if you are over 50 years old). You may choose a Roth IRA instead. You won’t be able to write off the investment now, but your money will grow tax-free, so you won’t have to pay taxes on the gains. Check with your accountant, fiduciary, or a trusted advisor. If you are worried about making ends meet, you can start with a smaller % and work your way up to 10% by adding 1-2% every 4 months. This will buy you time as you either look for ways to cut expenses or use that next pay raise to get you to 10%. Why pay yourself first? Compounding interest is our hero. Earning interest on interest on interest and so on. Check this out: $150 invested monthly at a modest 5% return, will grow into over $225,000 in 40 years. $150 invested each month for 40 years at 10% annual rate of return will grow into over $900,000. $150 per month for 50 years at a 10% annual rate of return and you're looking on over $2,500,000! $300 invested each month for 50 years at a 10% annual rate of return = over $5,000,000!!! Where can you cut expenses to save $150-300 per month? Phone bill, cable bill, eat out less? Find a way! Even better: $1500 per month ($18,000 per year) at 10% annual rate of return will grow into over $9mil in 40 years, and over $25mil in 50 years!!! So you can see how those extra 10 years at the end make a huge difference. That's compound interest baby! And hey, if you only get a 5% annual rate of return, you’ll still be pretty stinking rich by retirement. So save those bonuses. Let's get this done! Wondering how to get it all going? Where to invest? A fiduciary can help set you up for retirement. 3) Buy a Home – because they say you can’t get rich renting. Who are "they" you ask? Well, I'm not sure, but they own a home and they have a much greater net worth than the average renter. Aside from the real estate bubble that burst a few years ago, home values typically increase by an average of 6% per year. Now is a great time to buy with interest rates at historic lows. Personally, I would look for a pre-foreclosure or something in need of a little TLC. You can add a lot of value to a property in a short period of time. This is my personal opinion (and experience). Do your homework. I also recommend a 15 year fixed rate mortgage. More on this below. For now, check out Zillow's Rent vs. Buy Calculator. It will show you how many years it will take before the cost of buying equals the cost of renting - the breakeven horizon. 4) Stay Out of Debt. Debt = compound interest in reverse. The bank gets rich while we live paycheck to paycheck. I’ve tried that style of living. Gets old after awhile. Not cool. If you can’t pay for it, in full, without negotiating in your brain whether or not you can afford it, you can’t afford it. As I said in Deciding to Thrive, “Spending more than you earn and making up the difference on credit cards gives you a negative inner voice that makes it tougher to focus on business or family.” (Chapters 8 and 9 are your user manual for money) Debt happens. But why? Think about how our society views money. The national debt has increased by about $500,000 since you started reading this blog. What message does that send to our society? Student debt happens too. Some studies state that the average college student has over $2500 in credit card debt while 10% have more than $7000 in credit card debt. Trying to pay off $7000 in credit card debt at a typical 20% rate by making the minimum payment will take over 30 years and cost more than $20,000! And, unfortunately, I’m speaking from experience. At one point, in my twenties, I had six different credit cards to keep track of, so six different payments had to be made on time. Had I continued I would have been destined to work for Visa, Discover, MasterCard, and American Express forever. The other thing about being debt free is that it allows you to be a giver. If you are worried about paying off the mortgage in 15 years because you’ll lose the benefit of writing off the interest on your debt, I’d advise you to pay it off and then donate the same amount you were paying in interest to charity. Which, by the way, is also tax deductible. Look for 501 (c) 3 charities like the Children’s Dyslexia Centers (which is where my wife and I have decided to donate 100% of the money from our book sales). Tips on crushing your debt: - Create a spreadsheet of your debts. Include your monthly payments, the payoff, and goals to pay off your debt. Meaning, what day will you completely payoff that first card/debt? How about the second? How about all of it? - Start with the smallest debt first. Each card you get rid of constitutes a victory. - Stop with the instant gratification. While you are paying down debt, if you can’t pay cash, don’t buy it. - Look at your statements weekly, not once per month. This way there will be no surprises. - Keep attacking the debt until it’s gone. You can do this! 5) Dream Big. Victor Hugo said, “There is nothing like a dream to create the future.” Money is a vehicle to achieve what we want in life. Every single person reading this has the opportunity to launch their life by the actions they take from this point forward. I want you to be rich. You can get motivation from this blog if you can see how your actions get you closer to your dreams. The Decision happens in a moment. Every moment we are deciding. Deciding between weak thoughts and strong thoughts. Deciding to Thrive reminds me to shove the weak thoughts out and to fill my brain with strong thoughts. We attract what we focus on. If you choose to Decide to Thrive in the moment, how powerful is your life going to be? How powerful will you become as Deciding to Thrive becomes a habit?  "After reading over 200 books on leadership, self help, coaching, and mentoring I finally put it all together in one book. Deciding To Thrive is the distillation of what I learned about the nature of happiness, the meaning of success, the purpose of money, and the all-essential 'why' that helps great entrepreneurs create companies." - John Wasserman

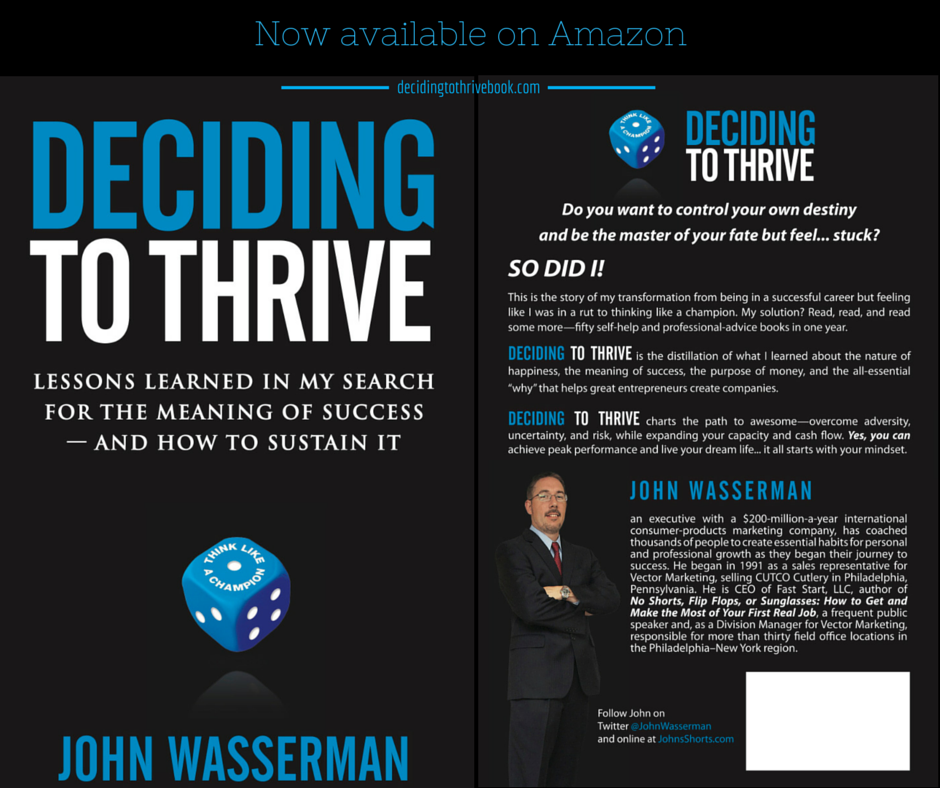

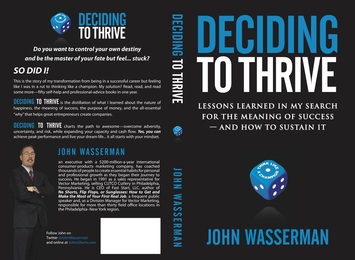

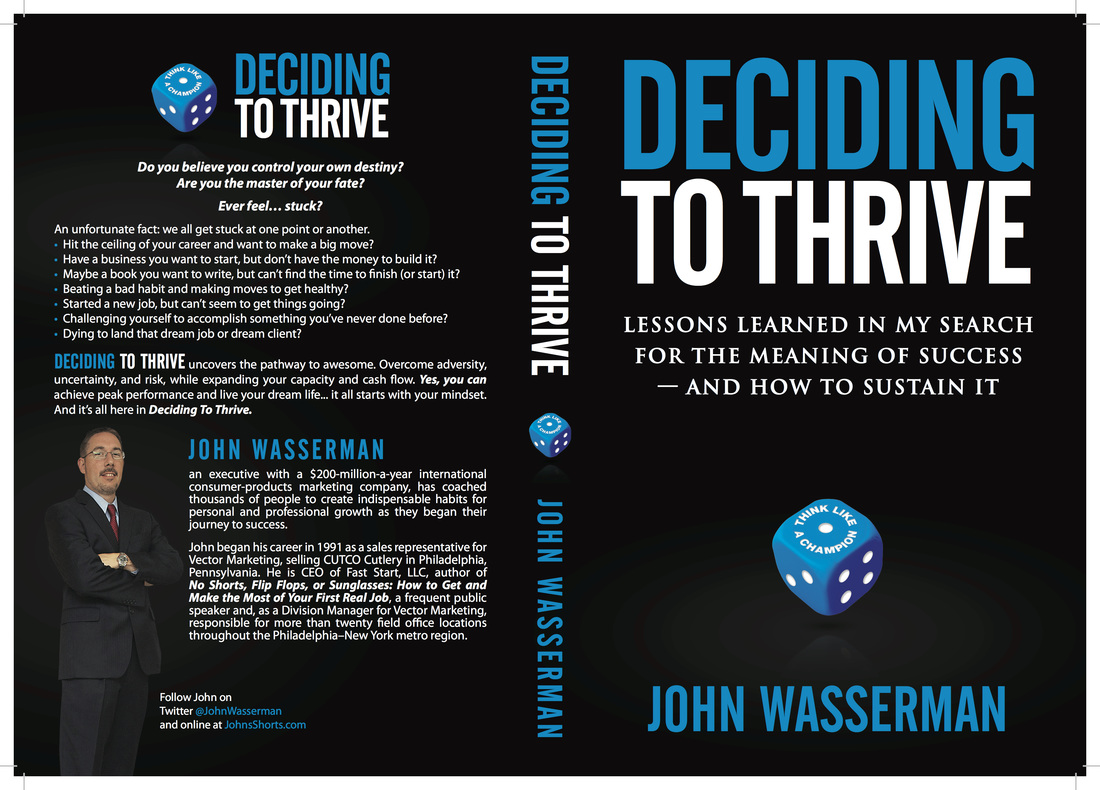

Author John Wasserman is an executive with a $200-million-a-year international consumer-products marketing company. He has worked with thousands of 18- to 25-year-olds teaching them the basics of business: how to prepare, look for, find, and make the most of their first "real" jobs - the ones that don't require hair nets or rubber gloves. John began his career in 1991 as a sales representative for Vector Marketing, selling CUTCO Cutlery in Philadelphia, Pennsylvania. He is CEO of Fast Start, LLC, a frequent public speaker and, as a Division Manager for Vector Marketing, responsible for more than twenty field office locations throughout the Philadelphia–New York metro region. After reading over 200 books on leadership, self help, coaching, and mentoring I finally put it all together in one book. Deciding To Thrive is the distillation of what I learned about the nature of happiness, the meaning of success, the purpose of money, and the all-essential "why" that helps great entrepreneurs create companies. The keynote was a blast to deliver at Vector Marketing's annual Strategic Leadership Conference in Atlanta. The Deciding to Thrive book is available on Amazon. 100% of the proceeds go to the Children's Dyslexia Center.   Today is the day! "Deciding to Thrive" is now available on Amazon! Here is the link. After reading over 200 books on leadership, self help, coaching, and mentoring I finally put it all together in one book. "Deciding to Thrive: Lessons Learned in My Search for the Meaning of Success - And How to Sustain It". Every penny the book generates will be donated to Children’s Dyslexia Centers, Inc A charity I am quite passionate about. Anything for the kids, right? Studies show that about one in five kids have some form of dyslexia. I know we can make a difference. Deciding to Thrive will have a profoundly positive impact on those that read it. A transformation for some, from being stuck to being successful and happy. And for others, the path to a dream life. Sincerely, John   Written by special guest blogger Elyssa Andrus John Wasserman wants to help you get a job. Yeah, you. A Philadelphia-based division manager for Vector Marketing, Wasserman has spent more than two decades recruiting and training college students. In that time, he’s interviewed thousands of people for their first “real” work experience. He knows a thing or two about what it takes to go from résumé to interview to wow-I-feel-like-a-grown-up because I wear a suit to the office. In his book, “No Shorts, Flip Flops, or Sunglasses – How to Get and Make the Most out of Your First Real Job,” Wasserman shows how to avoid some common job-search mistakes. 1. Putting all your eggs in one basket An interviewer can get thousands of resumes and pick three to review, says Wasserman. Do you want to boost your odds of someone actually taking a look at your credentials? Then you need to get those credentials to as many companies as possible. “Don’t put all your eggs in one basket,” he says. “Your goal shouldn’t be to find your dream job as your first job. What you need is experience. Go after the experience and upgrade to your dream job in the future.” 2. Unpolished résumé Don’t let some dumb grammatical error screw up your chances of scoring an interview. Have someone with legit editing skills review your résumé for accuracy, correct grammar, and completeness. And don’t be THAT GUY (or girl) who sent out a résumé with no contact information. You need to make it ridiculously easy for interviewers to find you.  3. Inappropriate attire for an interview “Leave your leopard print jumpsuit at home,” says Wasserman. Same with big, flashy earrings, short skirts, or grungy-looking clothes. Men should wear a tie to an interview. Ladies should wear a blouse with sleeves. (Armpits aren’t professional.) Dress better in your interview than you would dress for work every day. The interview is the time to be impressive. “You aren’t Mark Zuckerberg,” he says, “You can’t just show up in a T-shirt.” 4. Don't be gimmicky in the interview So you’re awesome. Of course you are. And any position you take? Clearly, you’re going to rock that job. If you’re considering bringing an actual rock with your résumé, think long and hard about the cheesiness factor. “You want to be memorable for your skills, not gimmicks,” says Wasserman. Really, you’d be surprised at the things people do in an attempt to stand out that are actually a turn off. 5. Inadequate preparation I bet you’ve heard this before. Take some time to visit the company’s website before the interview. Put together some intelligent questions. “You have to do your homework before you go to the interview,” says Wasserman. Take an honest, sincere interest in the company. Often you’ll find interviewers will take that same sort of interest in you. 6. Involving your parents In his 20-plus years on the job, Wasserman says he’s seen parents call to set up interviews or negotiate pay for their children too often. And that’s all kinds of wrong. Leave your parents out of your search for work, says Wasserman. It’s ok for them to help you in your decision making process. But remember, it’s YOUR decision. Involving them in the actual interview can be a huge turnoff to recruiters.  7. Acting arrogant or unprofessionally in the interview No matter how great that party was last weekend, keep that information on the down-low, says Wasserman. (Way, way down-low.) Have a firm handshake, wear a big smile, and leave any trace of arrogance at the door. Instead, be honest and polite to everyone you meet at the company. “You are interviewing the moment you walk into the building,” he says. “Your goal is to get the interviewer — and everybody you meet— to like you.” If you are polite and enthusiastic, chances are they totally will. Remember, the person that greets you could be a decision maker, too. See original blog post on this topic here.  Elyssa Andrus is an author, speaker, parenting columnist, and TV presenter. A longtime print journalist, she has worked for the New Era Magazine, BYU Magazine and most recently the Daily Herald newspaper in Provo, Utah, where she was the features editor for 10 years. She is the author of the book “Happy Homemaking” (Cedar Fort, 2012) and contributes to the popular KSL-TV lifestyle show “Studio 5.” Elyssa has a master’s degree in journalism from Northwestern University and is a former adjunct professor of communications at Brigham Young University. Her parenting column “Because I Said So” (co-written with Natalie Hollingshead) runs Mondays on Utah Valley Magazine’s website, UtahValley360.com.  Looking for resume tips? Check out John Wasserman's blog: 7 Resume Blunders You Can't Afford to Make. Also, check out John Wasserman's latest book: Deciding to Thrive: Lessons Learned in My Search for the Meaning of Success - And How to Sustain It. “That lesson has helped me advance in my field for two decades with a company that I love and lifestyle I cherish.” - John Wasserman  This is the book I've always dreamed of writing. I poured my heart and soul into it. I've gotten some great feedback so far. I believe this book will make a difference. Read the pic below to find out more. Every penny the book generates will be donated to Children’s Dyslexia Centers, Inc. Every penny matters to these kids. The book will launch on Amazon on July 21st. Set a reminder. Save the date. EMAIL ME and I will send you Chapter One.  John Wasserman, an executive with a $200-million-a- year international consumer products marketing company, has coached thousands of people to create indispensable habits for personal and professional growth as they began their journeys to success.

John began his career in 1991 as a sales representative for Vector Marketing, selling CUTCO Cutlery in Philadelphia, Pennsylvania. To date, John has made over $75 million in career sales. He is CEO of Fast Start, LLC, author of No Shorts, Flip- Flops, Or Sunglasses: How To Get And Make The Most Of Your First Real Job, a frequent public speaker, and, as a Division Manager for Vector Marketing, responsible for more than thirty field office locations throughout the Philadelphia–New York metro region. He also maintains a blog on personal and professional growth at JohnsShorts.com. He and his wife, Gitana, have two children, Jack and Anastasia, and live in the Philadelphia suburbs. Proceeds from John’s speeches and the sales of his books support Children’s Dyslexia Centers. |

Johns Shorts

by John Wasserman About the Author

Archives

October 2020

Proceeds benefit Children's Dyslexia Centers

|

RSS Feed

RSS Feed