I love being an entrepreneur. And like most entrepreneurs, I started out with nothing. I also had to figure out the money game with little help. I lived paycheck to paycheck throughout my early and mid twenties. I bought myself a two-seater sports car (MR2) with T-tops for my 23rd birthday, with nothing down of course. It was so bad in the snow that I tacked on a lease for a Pathfinder SUV. My combined payments were over $800 per month (slightly higher than my apartment rent at the time). Then one day I upgraded to a Hummer H2. I’d catch a wave from other H2 drivers, while total strangers would wave their middle finger. I did love that truck though. I justified the $65,000 expense because it weighed over 6000 pounds and I was able to write it off as a business expense. Finally I got smart, set some financial goals, started reading books and magazines about money, listened to audios, and solicited the advice of an advisor. The biggest lesson I learned... You have the power of choice. Financially, with every dollar you make, you hold the power to choose your future. You can choose to live a few paychecks away from financial ruin or travel the path to be financially fit. I also learned that you are not the car that you drive. Rather your spending habits reflect who you are. Poor people simply have poor spending habits. Below are 7 steps to help you on your journey to financial freedom, an Action Plan, and a snapshot of how I set up my bank accounts as an entrepreneur. 1) Create a Written Game Plan Ok, so you know the drill. Every month you put it all into excel or Quicken or Mint.com or scribble it on paper. List all of your expenses for the month and don't forget to include a category for savings. The problem I’ve found is that most people think it really is a once a month project. However, most wealthy people look at their budget weekly, or even twice per week. Log in your expenditures twice per week and re-evaluate where you are. This way you can right the ship before you end up at the wrong port. If you don't make this simple exercise a habit, you may find yourself cruising towards Someday Isle. You know, Someday I’ll get a grip on my finances, Someday I’ll save for retirement, Someday I’ll work on my budget. Your budget will allow you to project where you are going, otherwise you will never get there. Keeping track of your expenses each week will help you avoid any surprises. After teaching thousands of students about how to win with money over the past two decades, I’ve found that most people live their financial lives by looking over the stern instead of charting a course to move ahead. I’ve messed this up more than once. Luckily I didn’t run into an iceberg and sink my ship. I can’t tell you how many times I would get to the end of the month and ask, where am I? How did I get here? What happened? You have to look forward. Where there is no vision… By the way, a budget doesn’t mean you can’t have fun anymore. Just add a line for Fun in your monthly budget. It’s a written plan that charts the course to where we all ultimately want to be…Paradise Isle. And look at it weekly, not monthly. It’s ok to make changes to the budget when you find yourself off course. 2) "Act Your Wage... you have to live on less than you make, you are not in Congress.” – Dave Ramsey You will not prosper spending more than you make. While I did have a blast at times doing so, my wife reminds me that we didn’t really enjoy living that way. Choosing to live paycheck to paycheck to drive fancy cars; buying expensive things that we have since had to replace; and keeping up with the pseudo rich as if we had an unlimited supply, added way more stress to our already hectic lives. Acting rich, living on borrowed money…it’s a terrible plan. That’s what most people do, but you don’t want to be most people, most people do not retire the way they had hoped. We found a better way. It’s so much easier to save money when you aren’t paying Visa for your lifestyle. I know, I know… it’s “everywhere you want to be”. But, it’s the expressway to Someday Isle. That’s not where I want to be, how about you? 3) Get and Stay Out of Debt When you don’t have any payments you don’t have any distraction. At one point, in my twenties, I had six different credit cards. It’s not much fun working to pay off debt. I thought I was destined to work for Visa, Discover, MasterCard, and American Express forever. According to Dave Ramsey's book, The Total Money Makeover, when interviewed, the Forbes 400 (the 400 wealthiest people in North America), 75% said that the #1 way to become wealthy is to get and stay out of debt. No car payments, no student loans, no credit card payments. To be debt free. What would it feel like to have no payments? Think about how that resonates. When you don’t have any payments, it’s a lot easier to become wealthy. If you have debt, it’s time to make a plan. Put it all on a spreadsheet and get to work. There are several versions of the debt repayment plan called the Debt Snowball. You can either start with the highest % rate or, and I find this much more exciting, start with the smallest debt first. Ramsey suggests paying the minimum payment on everything but the smallest debt. Then attack that debt with any extra money you have. Once your smallest debt is gone, add that payment to your next smallest debt and attack. I love Ramsey’s explanation. “But, doesn’t it make more sense mathematically to start with the highest interest rate first? If you were good at math, you wouldn’t be in this situation, now would you?” By paying off the smallest debt first, when it’s gone, you get that win. It feels great! It gives you momentum! Set a goal to pay off your smallest debt by a certain date and GO!! You will have to make sacrifices. Don’t eat out. Work extra hours. Do whatever it takes. It WILL be worth it! Set a goal to pay off everything except the mortgage in 18 months or less. You would be surprised at what you can accomplish if you have a plan (aka. a budget) and do the Debt Snowball. You can ride the mortgage out; since you’ll need to start saving once your other debt is gone. Another great resource for a debt repayment plan is Credit Karma. 4) Save Money Once you’re out of debt (except the mortgage), Step one is an emergency fund. According to most experts, you’ll need at least three months of your household expenses in a savings or money market account. Six months is ideal, but three will get you started. Look at your necessary household expenses. The ones you would still keep if you lost your job. Think about it, if you lose your job, and you have no debt, and no car payments, and you have $18,000 in the bank, it’s a different kind of place to be. Step two, save up for the things you want or will eventually need to purchase. Now that you have no car payments, you can save that amount each month for your next car. How about the 20 year roof on your 14 year old house? You should be saving for it so you don’t have to go into debt to replace it in six years. In business that’s called a sinking fund. Your grandparents however, called it a rainy day fund. Step three, save for wealth building. Did you know that $100 per month invested in a decent growth mutual fund in a Roth IRA (which grows tax free) from age 30-70 would be worth about $1,000,000! I bet you blew more than $100 on "stuff" in the past 30 days. Do you even know where it went? If you looked at your budget weekly you would. 5) Invest

What to do after maxing out your Roth and SEP:

Many people are afraid to invest in real estate, but that fear comes from the unknown. Here it is as simple as I can make it. I. Knowledge a. “The ABCs of Real Estate Investing” - by Ken McElroy b. This book will teach you how to: • Achieve wealth and cash flow through real estate • Find property with real potential • Show you how to unlock the myths that are holding you back • Negotiating the deal based on the numbers • Evaluate property and purchase price • Increase your income through proven property management tools II. Identify an Opportunity III. TAKE ACTION! Incorporate or not? If you are an entrepreneur or self-employed, here are three reasons to be an LLC or S-Corp. (if you choose to be an S-Corp, one main difference is that you will have to file quarterly and annual meetings. You will need to record and report them). There is a tax advantage to incorporating if you are making at least $60k in profit or higher.

6) Get the Right Insurance Make sure you have the right insurance so you and your family are protected. This will actually be step one in the Action Steps you should take to get your financial life in order. Here are the 7 types of insurance that Dave Ramsey says you absolutely need.

Disability Insurance: Go to http://www.zanderins.com/disability/disabilityeducation.aspx and click on Instant Quote. This is where I got my Disability Insurance from. It's not expensive and very necessary. The need for disability income protection is crucial and is an essential part of your financial plan. It provides an income for you and your family if you have an accident or health condition that prevents you from working and earning a paycheck. ACCORDING TO THE COUNCIL FOR DISABILITY AWARENESS:

7) Leave it Better I have a goal to donate $1,000,000 to charity. If you develop the right core behaviors, you will have a lot left over to give. We all know how amazing we feel when we do something good for others. I was walking to an appointment in the Rittenhouse Square section of Philadelphia, not far from the Liberty Bell. I walked past several "down on their luck" people looking for a handout, but I was too caught up in my own schedule to stop. Then I made eye contact with an elderly gentleman with leather like skin. In his eyes I could see he was broken. I stopped in my tracks and handed him $40. He got a little teary eyed on me. I think it made his day. Giving is the most fun you can have with money. You can’t do that when you’re broke. If you need the $40 to pay for a tank of gas because you’re broke, then you can’t give…and that’s why this is the last step. You have to get your house in order first. For now, give something you may have more of. You can give time; there are plenty of charities that need your time. You can give blood; there are plenty of people in need of blood. You can even give encouragement; most of the world goes to sleep every single night without an ounce of encouragement. Leave people better. Action Steps:

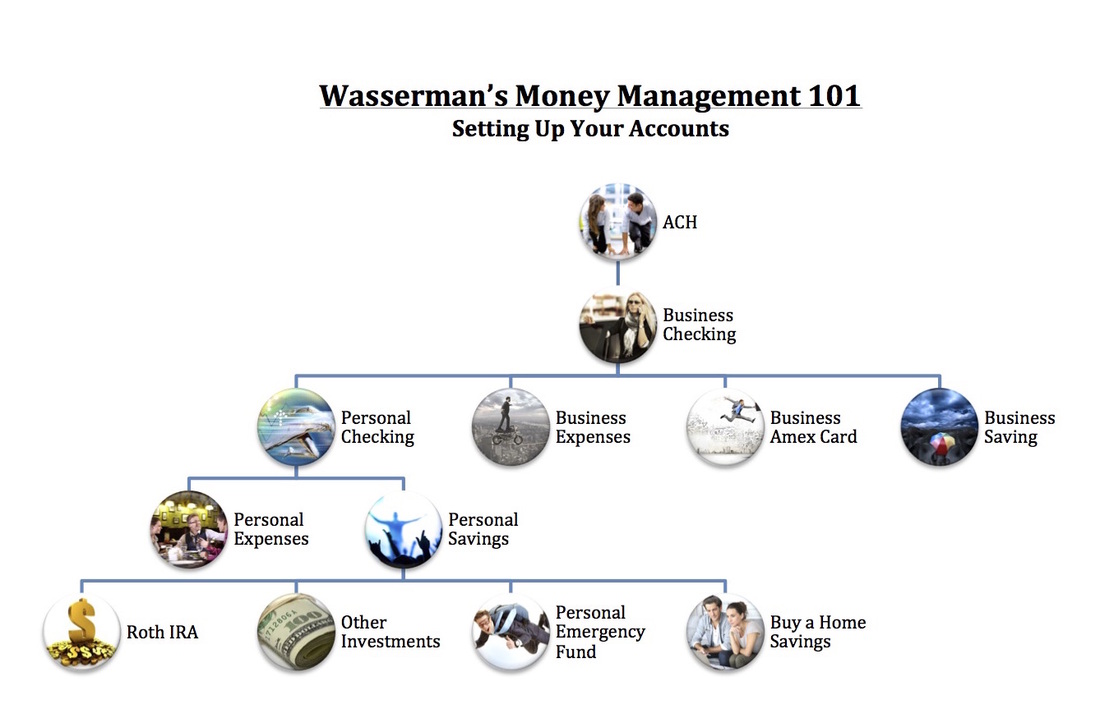

b. Fully funded Roth IRA (consult your accountant / fiduciary / advisor / or even your bank) c. Fully funded 401k, Single K, or SEP (or something similar – consult your accountant / fiduciary / advisor / or even your bank) 6. Save / Invest All Bonuses. a. See step 5. 'b' and 'c' first. b. This is a great way to save for a home or, if you have a home, for your rainy day fund (i.e. roof replacement) c. If steps 1-5 are maxed, think about using bonuses for other investment vehicles as discussed earlier. 7. Pay off your home early (and/or save for your kids college fund in a 529 Plan or a Coverdell) 8. Leave it Better.  I created this for the many small business owners I've coached over the past two decades. The ACH is the Direct Deposit to your company or business (or however your small business gets paid). If you are self-employed, it's important to separate your business account from your personal account. Then pay yourself from your business account (via written check) to your personal account. From Business Checking, you will also pay all of your business expenses. I do have an American Express card for my business, but you will notice that I don't have any credit cards personally. I like American Express because you have to pay it off monthly to continue to use it. And of course a Business Savings with 3 months worth of business expenses stashed away for a bad month or a slow quarter. From Personal Checking you will take care of your Personal Expenses. You will also transfer money into your Personal Savings each month. From Personal Savings you will fund your 3-6 month Emergency Fund, Investments, and save for a "Rainy Day" (i.e. new roof, car repairs, first home, etc.). - John Wasserman, Author, No Shorts, Flip Flops, or Sunglasses: How to Get and Make the Most of Your First Real Job For more on becoming financially fit, check out these blogs by Wasserman: Financial Fitness Starts Here Create a New Financial Paradigm Strengthening Your Financial Core  Disclaimer: This was written with love from my personal experience. I am not a financial advisor or fiduciary. Please consult the advice of a professional. And please consult your Doctor about exercise. I know this wasn't a blog on exercise, I'm just trying to cover all the bases. :)

3 Comments

|

Johns Shorts

by John Wasserman About the Author

Archives

October 2020

Proceeds benefit Children's Dyslexia Centers

|

RSS Feed

RSS Feed